Implied volatility is one of the most important variables used in option pricing models, including the well-known Black-Scholes Option Pricing Model. It reflects the market’s expectations of how volatile a financial asset may be in the future.

In options trading, volatility plays a critical role because it directly affects the price of option contracts. Higher expected volatility usually leads to higher option prices since there is a greater probability that the asset price will move significantly before the option expires.

Variables Used in Option Pricing Models

Most option pricing models rely on several key variables to determine the theoretical value of an option. These typically include:

- The current security price

- The strike price of the option

- The risk-free rate of return

- The time remaining until expiration

- The volatility of the underlying asset

When all other variables remain constant, the asset with the highest volatility will generally have the highest option prices. This is because greater volatility increases the likelihood that the option will end up profitable before expiration.

Why Volatility Matters in Options Trading

Many technology and Nasdaq-listed stocks historically show higher levels of volatility compared to traditional NYSE stocks.

For example:

- Technology stocks such as XIRC and AMGN often exhibit higher volatility levels.

- Traditional stocks like G and MRK tend to have lower volatility.

As a result, options on high-volatility stocks are usually priced higher, reflecting the increased uncertainty and potential price movement in those securities.

Measuring Volatility in Financial Markets

One common method used to measure market volatility is calculating the standard deviation of the underlying security’s price movements.

Standard deviation provides a statistical measure of how much the price of an asset fluctuates around its average value. However, this method mainly reflects historical volatility, meaning it looks at past price movements.

In many cases, the actual market price of an option implies a different level of volatility than what historical data suggests. This difference led to the development of the concept known as implied volatility.

What Is Implied Volatility?

Implied volatility represents the level of volatility that the market expects for an asset, based on the current price of its options.

Instead of relying on past data, implied volatility is derived directly from option prices in the market. If the price of an option is known, traders can input the other variables into an option pricing model and solve for the volatility value that matches the option price. This calculated value is known as implied volatility.

Because it reflects market expectations, implied volatility is widely used by traders to evaluate potential price movements and identify trading opportunities in the options market.

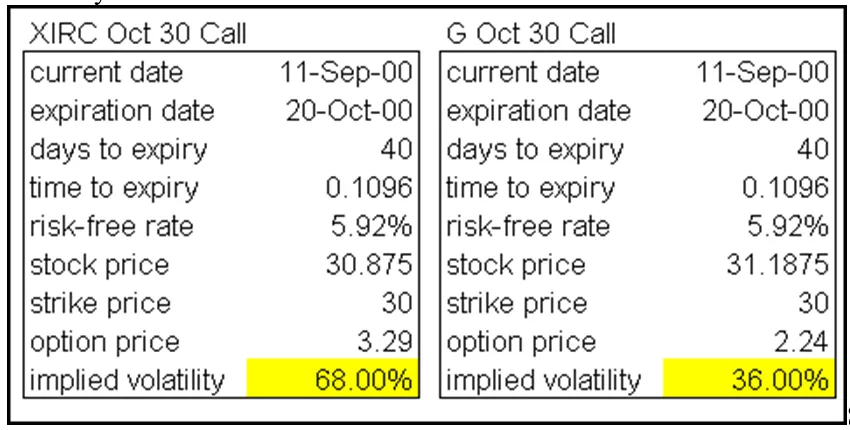

Example of Implied Volatility Impact

An example taken during trading on September 11, 2000 illustrates how implied volatility can significantly affect option prices.

At that time:

- XIRC was trading at 30.875

- G was trading at 31.1875

Despite having similar stock prices, the September 30 Call Option for XIRC was priced approximately 33% higher than the corresponding option for G.

In this case, most pricing variables were nearly identical except for implied volatility.

Using the Black-Scholes Model, the estimated implied volatility values were:

- XIRC: 68% implied volatility

- G: 36% implied volatility

This higher volatility level explains why the option on XIRC was priced significantly higher. Higher volatility suggests greater potential price movement, which increases the potential reward but also raises the level of risk.

In this example, the risk-free rate was calculated using the 60-day simple moving average of the 10-year Treasury note yield, while the time to expiration was determined by dividing the remaining days until expiration by 365.

Conclusion

Understanding implied volatility is essential for anyone involved in options trading. It provides valuable insight into market expectations and helps traders evaluate whether option prices are relatively high or low.

Since higher implied volatility generally leads to higher option prices, traders often analyze volatility levels to determine the best opportunities for entering or exiting positions.

By combining volatility analysis with option pricing models such as the Black-Scholes Model, investors can make more informed financial decisions when trading in derivatives markets.

You can now benefit from LDN company’s services through the LDN Global Markets trading platform, which provides advanced tools and market access for investors and traders worldwide.